Swiss Rhine Ports as a Gateway to Switzerland – Also for Cocaine?

May 4, 2026 at 7:59 AM

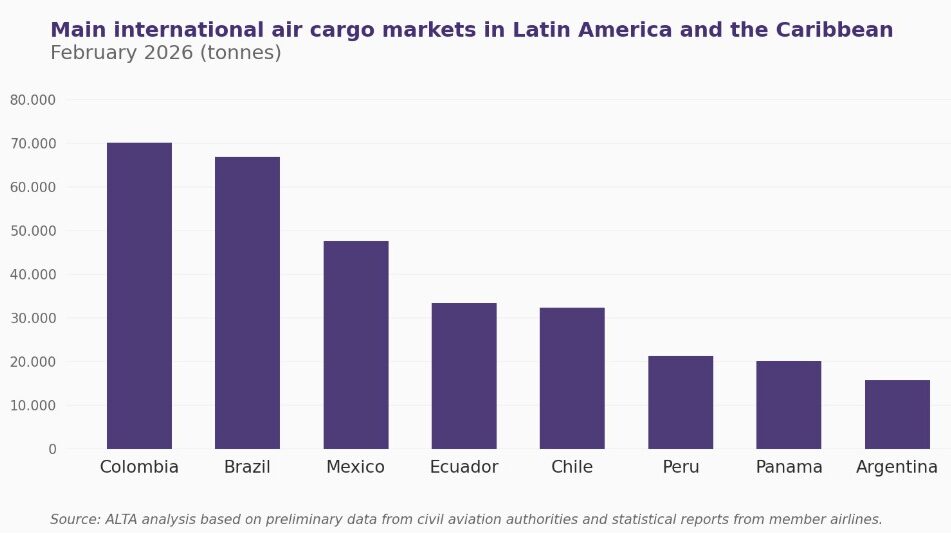

Colombia is Latin America’s air freight driver

May 4, 2026 at 8:37 AM

Worldwide air freight capacities and tonnages increased by another 3% in the last full week of April. This rise is partly attributed to seasonal factors and upcoming national holidays. At the same time, freight rates saw a slight increase as markets continue to adjust to the situation in the Middle East.

Flower exports drive growth

According to the latest weekly figures from WorldACD Market Data, the gross weight in week 17 (April 20 to 26) from Central and South America rose by 19% compared to the previous week. This increase is due to flower exports from key countries such as Colombia and Ecuador, which were shipped to the USA and Canada ahead of Mother’s Day on May 10. The 19% increase corresponds to the market growth in the same week of the previous year. Another significant increase in tonnages in week 17 was a rise of 3% from the Asia-Pacific region, driven by the upcoming Labor Day holidays in China and other countries around May 1. Tonnages from the Middle East and South Asia recorded a slight increase of 1%, while volumes from Europe and Africa stagnated, and tonnages from North America decreased by 2%.

Overall, global tonnages in week 17 were 9% higher than in the corresponding week of the previous year, with the Asia-Pacific markets showing an 8% year-on-year growth. Europe experienced a 20% increase, while Central and South America grew by 12%. In contrast, tonnages from the Middle East and South Asia fell by 3% and from Africa by 8% year-on-year, indicating ongoing challenges in international markets due to the conflict in the Middle East.

Capacity constraints persist

On the capacity side, the flourishing flower trade led to an 8% increase in capacities from the Central and South American markets in week 17. There was also a 5% increase from Europe, while capacities from the Middle East and South Asia rose by 3%. North America saw a 2% increase, and capacity from the Asia-Pacific region grew by 1%.

Compared to global air freight capacity in week 7, prior to the military confrontations between the USA and Israel against Iran, global capacity in week 17 was 3% lower. Capacity from the Middle East and South Asia had decreased by 26% compared to pre-war levels, while capacity in the Gulf fell by 46% and in the Eastern Mediterranean by 20%.

Prices continue to rise

The ongoing capacity constraints, combined with rising kerosene costs and availability issues, have resulted in air freight prices being significantly above pre-war levels and last year’s prices. In week 17, rates remained relatively stable, with an average increase of 2% in global spot prices (to $3.76 per kg) and 1% in full market prices (to $3.19 per kg). This means that global full market prices have risen by 30% year-on-year, while spot prices are about 45% higher than last year. Particularly high annual increases were recorded in the markets from the Middle East and South Asia (+65% to $4.65), North America (+60% to $2.65), the Asia-Pacific region (+41% to $5.11), Africa (+40% to $2.86), and Europe (+32% to $2.87). Spot prices from Central and South America increased by 12% compared to the previous year, averaging $1.92 per kg.

Although average spot prices from MESA to Europe decreased by 6% in week 17, they remain 73% higher than the previous year. Spot prices from Bangladesh stand at $5.15 per kg, representing a 55% year-on-year increase, while prices from Dubai have risen by about 160% to an average of $4.68 per kg.

{kind=link}