easyGroup launches “easyCourier” in Cyprus

Jun 5, 2026 at 12:41 PM

Tailwind Shipping registers “Panda 001” in Barcelona

Jun 5, 2026 at 1:01 PM

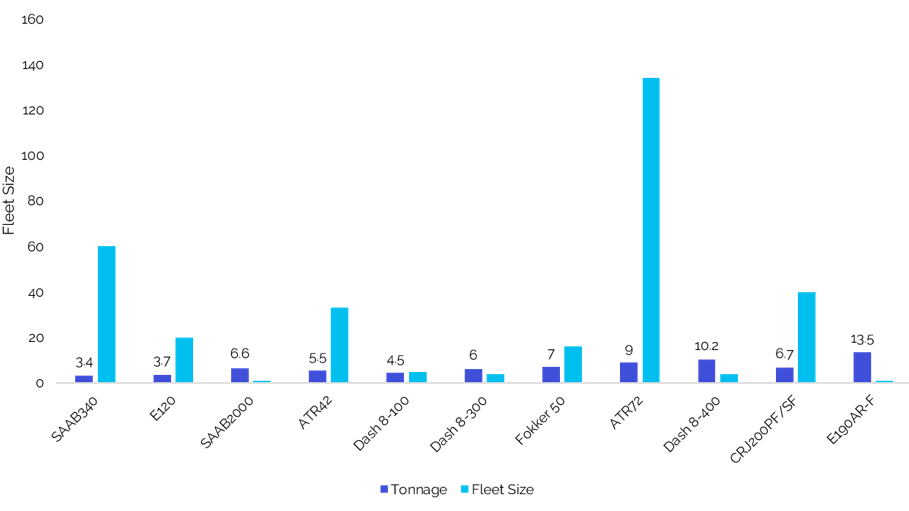

The fleet of regional cargo aircraft currently comprises 320 turboprop and jet freighters, offering a capacity between 3.4 and 14.3 tons. Approximately 50% of this fleet consists of the ATR72-200/210/500 and -600 series, which have a capacity of 9 tons. According to IBA Insight, 33 ATR42-300F/320F aircraft are in operation, characterized by long operating times and a strong global network. The fleet of SAAB340A/B/BPLUS freighters includes 60 aircraft, whose lifespan has now been extended to 80,000 flight hours, allowing for long-term use of these types, according to IBA. Additionally, EASA has approved the cargo model SAAB 2000, with IBA estimating that about 10 SAAB2000 will be converted into freighters.

Market development and conversion opportunities

A small number of converted Fokker 50F freighters are still in operation. The most realistic replacement options are used ATR72s. There is also demand for conversions of Dash 8-100 freighters. The age of the program is not a hindrance, especially considering the Extended Service Program (ESP), which allows for up to 160,000 cycles. De Havilland offers a simplified cargo package for the Dash 8/Q300. The Canadian operator Air Inuit has also undertaken a cargo conversion with an STC from Collins Aerospace, which includes the installation of a large cargo door.

In the jet sector, two types are represented: the CRJ200PF/SF (40 units) and the Embraer 190AR-F (1 unit), with the CRJ200PF/SF dominating the segment. The CRJ200SF features a large cargo door and is suitable for networks where speed allows for quicker turnaround times. An Embraer 190AR-F with a capacity of 13.5 tons is in operation with Bridges Air Cargo. However, demand for these models is very low, which IBA attributes to comparatively high costs for conversion and operation.

Market values and leasing rates

IBA has provided an assessment of market values and leasing rates for a selection of models. High maintenance costs and a limited supply have kept values stable. Leasing rates are not as dynamic due to sporadic demand in the cargo sector and a strong passenger market, where lessors often prefer more stable operators.

Outlook for the future of regional cargo aircraft

Despite their niche position, turboprop aircraft play a crucial role and will continue to do so in the future, especially on routes where the higher costs or capacity of larger jets cannot be justified. The ATR72 family is expected to dominate this segment, supported by extensive global services, successful conversion programs, and potentially strong passenger traffic. With a current fleet size of only 41 units, the regional jet cargo sector appears even more specialized. While IBA anticipates further conversions of CRJ200PF/SF, it expects this to be limited in scope. Demand for the Embraer 190AR-F is disappointing, as only one aircraft is in operation. Although this model provides a good capacity bridge between the largest turboprops and a Boeing 737, the market does not seem to have embraced these models, as reflected in the low number of orders.

{kind=link}

{kind=link}