WIESE and SAF develop forestry vehicle concept

Apr 30, 2026 at 8:03 AM

Cinquina expands electric fleet

Apr 30, 2026 at 8:54 AM

The global demand in the air freight market decreased by 4.8% in March 2026 compared to the previous year. This development is attributed to a challenging operational environment characterized by geopolitical tensions in the Middle East and seasonal effects. While Africa showed the best performance with an increase of exactly 7%, the Middle East experienced a dramatic decline of 54.3%.

International freight flows under pressure

International air freight traffic fell by 5.5% year-on-year. Airlines in the Middle East were particularly affected, suffering a decline of 54.2%, attributed to a deterioration in hub connectivity and network reliability. The overall capacity of the industry decreased by 4.7%, in line with the declining demand. The freight load factor remained stable at 47.9%.

Volatility in energy markets was also significant. The price of Brent rose by 43.1% year-on-year, while the price of jet fuel increased by 106.6%, reaching the highest level in over 23 years. These developments led to an increase in freight rates by 18.9% in an inflationary price environment.

Regional differences in freight performance

Regional performance in the air freight market was uneven. While Africa, Asia-Pacific, Europe, and Latin America and the Caribbean recorded moderate growth rates, these could not offset the dramatic declines in the Middle East. African airlines achieved the strongest growth, supported by bypass traffic. In Europe (+2.2%) and Latin America (+1.8%), there were smaller gains, while North America (-1.1%) slightly declined, indicating weaker transatlantic dynamics.

The situation in the Middle East posed the greatest obstacle to industry performance. The decline of 54.3% in CTK (Cargo Tonne-Kilometers) highlights the severe impact of the conflict on hub connectivity and aircraft utilization.

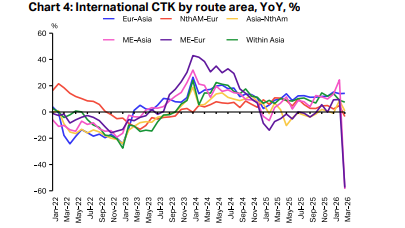

International trends and route analyses

International freight demands showed a clear geographical imbalance. While markets in Africa and Asia-Pacific (+5.5%) grew, airlines in the Middle East experienced the steepest decline. Route analysis revealed that the Europe-Asia connection had the strongest performance with an increase of 14.2%, while Gulf-connected trade routes were under significant pressure.

The demand for freighter aircraft proved to be more resilient than the demand for passenger cargo, which fell by 12.1%. This indicates that freighter aircraft benefited from operational flexibility and intercepted bypass flows on long corridors, particularly in Asian trade.

Outlook and economic conditions

Jet fuel prices rose sharply in March, significantly impacting the profitability in the air freight sector. Global manufacturing indices indicate that industrial activity remains in the expansion zone, although the momentum is slowing compared to previous months. Despite these challenges, the air freight industry remains on a stable macroeconomic foundation, even as growth momentum decreases from the peaks of previous years.

{kind=link}