Denny Jünemann new Managing Director of Rail4Captrain

Apr 2, 2026 at 1:09 PM

Hanes Australasia expands distribution center

Apr 5, 2026 at 9:03 AM

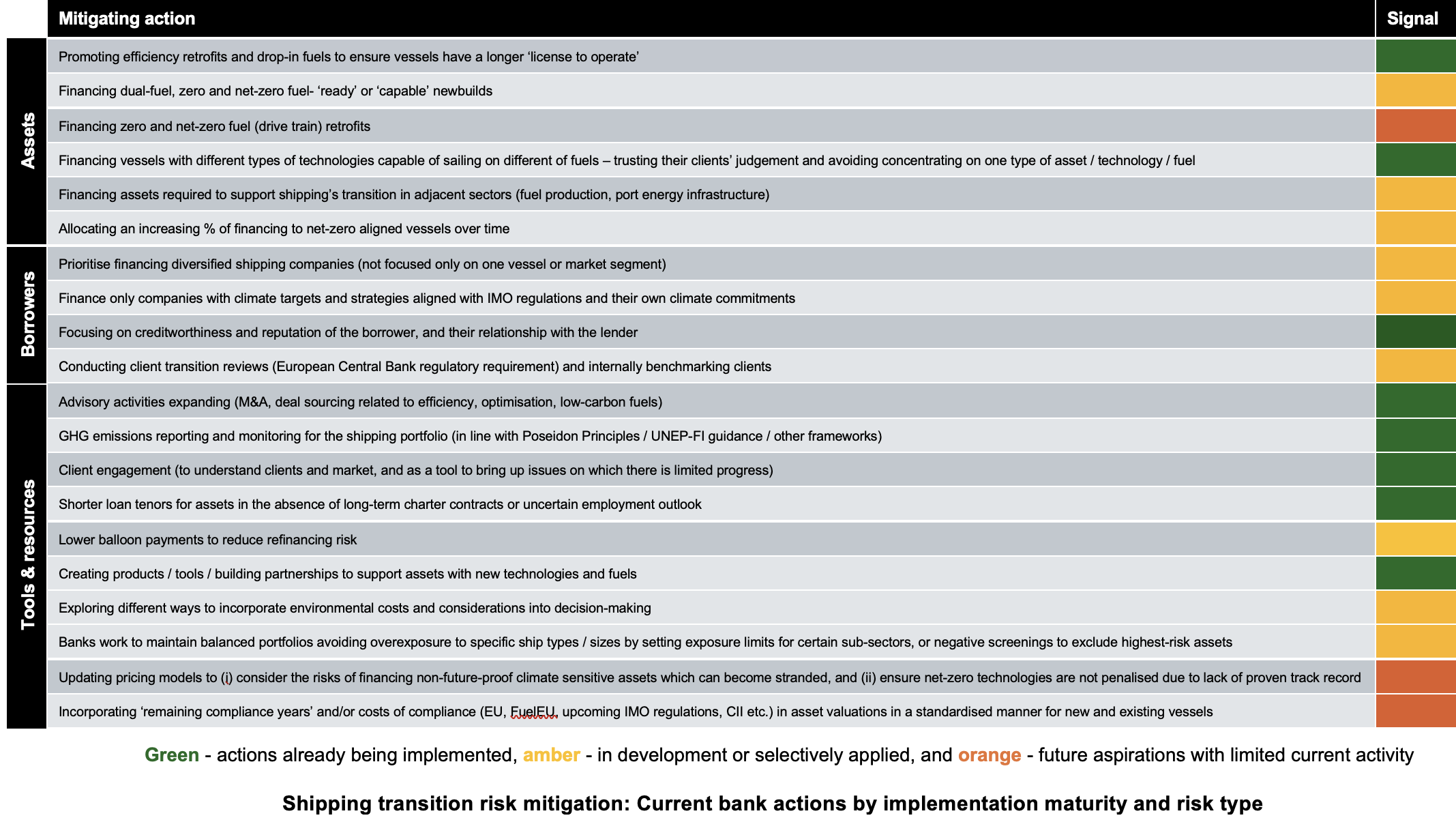

A recent study by the UCL Energy Institute and Strider Carbon examines the financial impacts of risks arising from the transition to more sustainable energy forms in shipping. The analysis shows that while banks are largely protected from direct losses due to climate-related risks, there are latent systemic refinancing risks stemming from the energy transition and stricter emissions regulations in shipping.

The investigation, titled “Exploring the Financial Impacts of Transition-Related Stranded Asset Risks,” highlights how climate-related value losses, such as when a ship is unable to comply with greenhouse gas emissions reduction regulations cost-effectively, can affect common financing structures in shipping. The study categorizes the resulting risks within traditional bank risk categories and evaluates the strategies currently employed by European financing institutions for risk mitigation.

Systemic Refinancing Risks in Focus

Prasanna Colluru, Managing Director of Strider Carbon, emphasizes that analyzing transition risks in conjunction with traditional credit risks can help banks better assess their shipping finance portfolios and strengthen their climate risk management strategies. The investigation reveals where existing debt structures are stable and where potential weaknesses exist that are not yet visible at the portfolio level.

The study notes that banks are generally protected from direct losses as long as no systemic shocks occur. This applies to both supply, when ships become economically unviable due to stricter emissions regulations, and demand, when the transition to renewable energy reduces cargo volumes for fossil fuel transport. In the financing mechanisms examined—including bilateral loans, ECA-backed facilities, and syndicated structures—a significant asset devaluation is required before banks incur direct losses. In all three structures, the equity of shipowners initially absorbs the losses while senior debts are preferentially repaid.

However, the study warns of the systemic refinancing risks arising from the discrepancy between typical loan terms of five to seven years and the operational lifetimes of ships of 20 to 25 years. This discrepancy allows individual banks to withdraw from transition risks before value losses occur at the end of the asset’s life. This leads to a collective action problem: if transition concerns cause multiple institutions to simultaneously restrict lending in the late 2030s, the resulting conditions could push recovery values below outstanding loan amounts, causing direct losses for the entire banking system.

Dr. Nishatabbas Rehmatulla, Principal Research Fellow and Co-Director of the Shipping and Oceans Research Group, highlights that modeling climate risks in shipping is complex and requires the integration of multiple variables. In the absence of rigorous, transparent, and common frameworks for capturing climate resilience, banks and other financiers may incorporate these considerations into assessments in an unsystematic manner, leading to blind spots that only become visible under stress.

{kind=link}

{kind=link}

{kind=link}